[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading text=”Market Commentary Update & the Banking System” use_theme_fonts=”yes”][vc_column_text]

This is Bob Barber of Christian Financial Advisors®. Yesterday morning all our advisors met to discuss the markets and what is happening in the present banking system. I asked one of our advisors, Don VandeVanter, to write a commentary on this matter. Don is a CPA and has over 20 years of experience as a Banking CFO of a large lending institution, including leadership during the financial crisis of 2007-2008. Click here to learn more about Don.

As always, feel free to reach out to Don or any of our advisors with any concerns or questions you may have by text or phone at 830-609-6986

[/vc_column_text][vc_column_text css=”.vc_custom_1678804562761{margin-top: 30px !important;}”]

What is happening with the Banks?

By Don VandeVanter, CPA

Written on March 13th, 2023

On Friday, March 10, 2023, the California Department of Financial Protection and Innovation closed Silicon Valley Bank (SVB), and the Federal Deposit Insurance Corporation (FDIC) was appointed its receiver. With over $200 billion in total assets, SVB is the second-largest bank ever to go into receivership. Signature Bank of New York (SBNY) also went into receivership yesterday, March 12.

The Federal Reserve, Department of the Treasury, and the FDIC made a joint announcement yesterday evening that they “are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.” The Federal Reserve also announced it will “make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.” The Federal Reserve has coined this program the “Bank Term Funding Program.” The full transcript can be read here:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20230312b.htm.

The FDIC has assured all depositors to SVB will have full access to their money beginning today, March 13, including those deposits in excess of $250,000.

Despite these steps, most financial institutions are seeing their stock valuations decline, some of them very significantly over the last week. The losses at SVB and SBNY were not driven by bad lending decisions but rather by bad asset management. Over the course of 2020 and 2021, as the Federal Reserve and the US government poured trillions of dollars into the financial system, banks were flooded with deposits. In return for the oversupply of money, banks did not have to pay much interest at all for those deposits, with savings rates of less than 0.10 percent and 1 year CD rates of less than 1 percent. As the Federal Reserve began its fight against inflation in March of 2022, Treasury rates began to increase substantially. Investors saw an opportunity to earn some yield on their money and began withdrawing their deposits at banks to invest in Treasuries and other securities that had yields in ranges of 2 to 4 percent. Banks, such as SVB and SBNY, did not have the cash reserves to meet the demand for deposit withdrawals, so they had to begin liquidating their investment portfolios (many of which were securities bought in 2020 and 2021 with low yields) and incurred significant losses (because of the rise in interest rates). SVB disclosed last week losses on the sale of securities in excess of $1.8 billion. More information on the demise of SVB can be found here:

https://www.cnbc.com/2023/03/10/silicon-valley-bank-blowup-highlights-deposit-risks-vs-treasurys.html.

Bank analysts see the potential for more runs on banks in the short term but many believe that these banks should have time to raise cash levels to meet these demands. “The question is for depositors with balances over $250K, how comfortable are they with their bank and do they attempt to diversify?,” said Citi analyst Keith Horowitz. “We believe regionals with less diversified and large uninsured deposit bases are at risk of deposit flight but not at the speed of SVB and they should have time to tap wholesale funding markets (such as FHLB) and raise cash levels,” he added, referring to the Federal Home Loan Bank system. This is where the Bank Term Funding Program announced by the Federal Reserve should help these banks raise cash without booking losses.

At Christian Financial Advisors®, we have reviewed the portfolio of Certificate of Deposits we have purchased recently for our clients. We do not have more than $250,000 invested on behalf of any one of our clients in one financial institution but have these investments spread over many financial institutions. We would encourage any of our clients with cash holdings greater than $250,000 at any one financial institution to review the financial reports of that institution to see if they have any significant exposure in their marketable securities that may hinder them from being able to meet any demand on their deposits.

On a bright note, the recent sell-off in stocks, coupled with the news that the average hourly earning rate increase came in much lower than expected, has led to a significant increase in the value of short-term marketable securities, which may in itself help some of the banks alleviate their exposure in this area. Many are now speculating that the Federal Reserve may slow the increase in rates as well. In addition, the federal government, including President Biden, is making announcements that the US banking system is safe.

https://www.nbcnews.com/politics/politics-news/biden-deliver-remarks-silicon-valley-bank-shutdown-rcna74622

Written by:

Don VandeVanter, CPA

Approved by:

Bob Barber, Founder

Shawn Peters, Vice President[/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

Market Commentary: 2022 Recap and 2023 Forward

By Bob Barber and Shawn Peters

As we begin 2023, we look back on 2022 and look forward to this new year. Last year was volatile for the stock markets as they entered into a Bear Market (a 20% decline from previous highs) in June. Today as I write this, we are squarely right in the middle of a Bear market that could last another 6-7 months based on average Bear markets lasting 13 months.

What caused this present Bear market?

This present Bear market decline is mostly from speculation that higher interest rates brought on by the Federal Reserve could cause a severe recession which so far has not happened. December increased this speculation fear, with the federal reserve raising interest rates another 50 basis points or ½%. The Fed is doing this to lower inflation and to normalize interest rates after the artificial lows during the COVID shutdown to stimulate the economy. We’re all paying the price with massive inflation caused by the Fed’s artificial stimulus and government stimulus checks.

Interest Rates

One year ago, the Fed funds rate was at zero percent. Today, the rate is 4.5% higher than a year ago. The market consensus is that the Fed will only raise interest rates another ½ to ¾ percent more, topping the Fed rate at 5 to 5.25% in mid-2023, then either stopping rate hikes or even pivoting by lowering rates.

Mathematically the first 4.5% of interest rate increases dropped the overall stock markets by approximately 20-25% or an average of 2.2% for every ½ percent the Fed raised rates. With just ½ to ¾ percent left to go, the markets should drop at most another 2-5%, based on mathematics. If it does drop more than this, it’s an overreaction and creates buying opportunities. Think of the Fed’s interest rate increases in miles. If you had a 500-525 mile trip to drive and were at 450 miles already, you are very close to your destination. This is the case for the Fed.

Real Estate

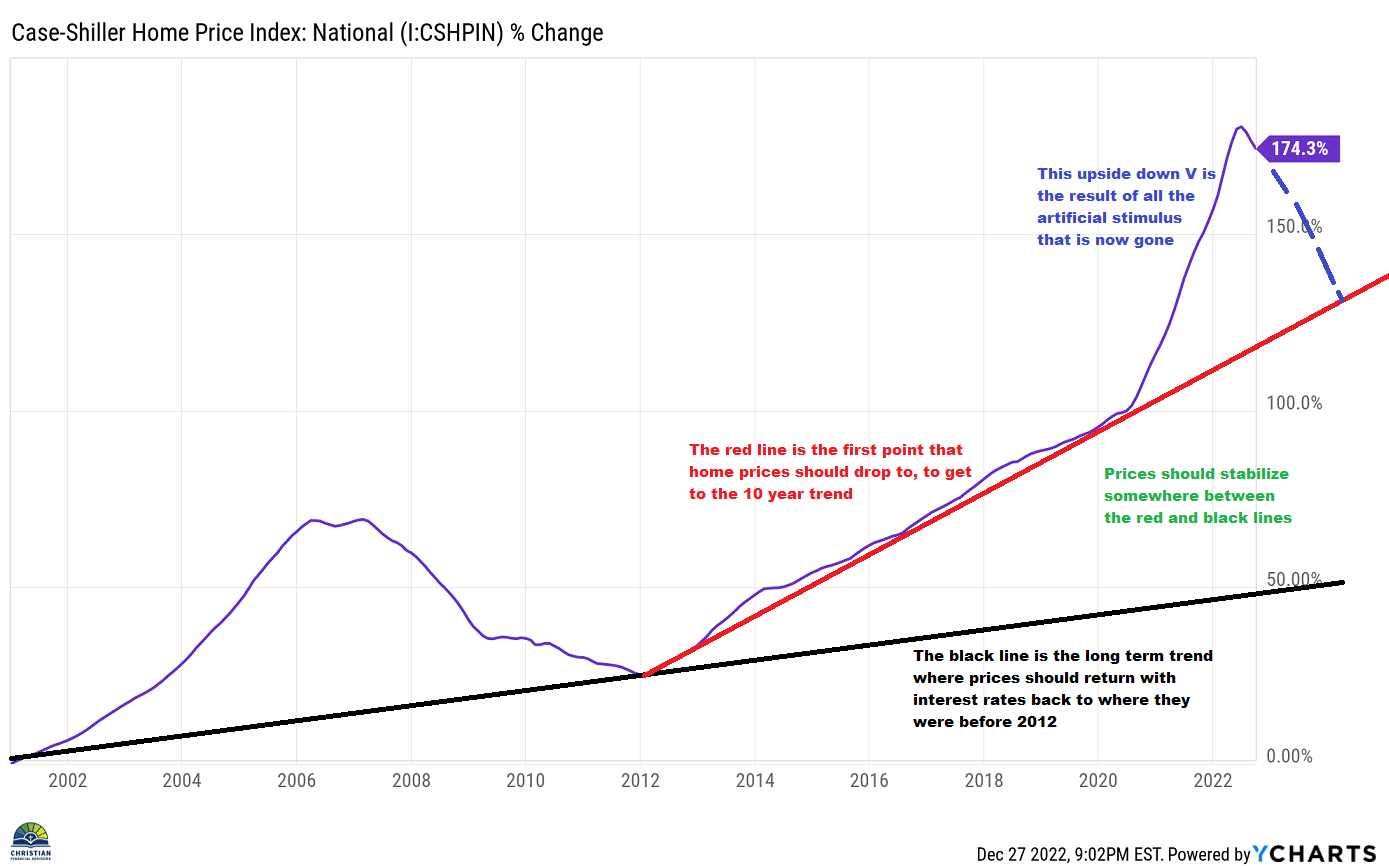

The area that interest rates have affected the most and will continue to affect the most is real estate. A year ago, a $3,000 monthly mortgage payment could finance a $750,000 home. That same payment will now only finance a $450,000 home at today’s rates. A $2,000 payment a year ago could finance a $450,000 home; today, it’s $300,000. From a mathematical perspective, if interest rates stay where they are, then today’s home prices need to fall enough to equalize the payment. Yes, you’re reading this correctly. That $750,000 home a year ago needs to drop to $450,000 to equalize the same payment as a year ago. A $450,000 home a year ago needs to drop to $300,000. It’s just math, and like my dad used to say, figures don’t lie. If you’re looking to buy a home today, please wait! wait! wait! I have repeatedly said that home prices were artificially high since late 2021, and now it’s proving right. It’s just math! Please review the chart I have included below.

Recovery and History

Taking all the above in consideration, we will most likely see another six months of pain in the stock market, but nothing like the first six months of 2022 when over 90% of the drop occurred. As I said above, with just 50 to 75 basis points or ½ to ¾ percent of interest rate increases left, the markets should drop no more than another 2-5% based on mathematics. Then I believe we are in for an L-shaped, possibly U-shaped recovery in the second half of 2023. All our portfolios are positioned well for the current market conditions.

We made some good buys in 2022 with the cash we took out of stocks in October of 2021 when the markets were at all-time highs and still have considerable cash left to buy more which we are doing in small increments when the markets overreact.

2022 was the worst year for the stock markets since 2008, but it was not worse than 2008. Markets rally after bear markets. For example, in the two years following the 2008 downturn, the S&P 500 rallied 39.23%, and the Nasdaq (QQQ) rallied 83.12%. Will history repeat itself? Maybe, maybe not, but it’s worth considering.

With very little left for the markets to drop now, in my opinion, I feel it is a good time to invest any cash on the sidelines by dollar cost averaging cash into the markets over the next several months before the markets possibly start to recover. When the markets get any indication that the Fed is done raising rates (or is considering pivoting to lower rates), the recovery could be so quick that any cash not invested will miss out on “the sale” that stocks are having now. The time to buy stocks is when they are “on sale,” but for some reason, stocks are the one thing people like to buy high and sell low. You should do just the opposite: buy low and sell high.

Looking Forward

Inflation should stabilize in 2023 as things continue to return to normal. In 2020, 2021, and 2022 we dealt with Covid, the Ukrainian war (which still continues), the cascading effect of supply chain disruptions, a new car shortage for lack of computer chips, etc., like we had not seen in 40-50 years. All of this is returning to normal, which is a very good thing.

In the Bible, Ecclesiastes 3:1-8 tells us there is a time for everything; war, peace, prosperity, famine, etc. This scripture assures me that the bad and good times are always temporary, so enjoy the good when they are here and rest assured that in the bad times, the good times will return.

God is in control, and we must trust Him regardless of circumstances.

If you have any questions or comments, we would love to hear from you. As always, we can be reached by phone or text at 830-609-6986 during regular business hours. You can also email us (click here) or set up an appointment (click here).

We also invite you to watch and subscribe to our weekly YouTube videos (CLICK HERE) or listen and subscribe to our weekly Podcast (CLICK HERE) on Christian Financial Topics.

Happy New Year from Christian Financial Advisors®.

Bob Barber – CEO and President

Shawn Peters- CCO and Vice President[/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]First Things First

September 13, 2022 was the worst day of the year for the overall markets. This was caused by news that inflation was higher than expected and concerns that the Federal Reserve will continue to raise rates. Then on the very next day, on September 14th, news was released indicating wholesale prices had decreased.

We are pleased to report that we have not received any panicked calls or messages from clients this week regarding the markets as our clients understand this is only a short-term correction and a normal part of the investment process.

The Positives

Many commodities that increased during the pandemic have dropped considerably during the last few months, another indication that inflation has peaked. For example, over the last six months, prices for Lumber is down 60%, Copper is down 18%, and Steel is down 20%. The August Consumer Price Index (CPI) was up 8.3% versus the expected rate of 8% but Inflation peaked in June at 9.1% and has decreased in both July (8.5%) and August (8.3%). So inflation is heading in the right direction by declining.

With significant increases expected soon in the base interest rate from the Fed, expect to see decreases in the price of homes in some areas by as much as 30%. This needs to happen to get real estate prices in line with where they should be.

The Negatives

The NASDAQ and S&P 500 entered into Bear Market territory in May and June which is a drop of at least 20% from previous highs. The average Bear Market last around 13 months so we could see another 9 months of this. Nobody likes Bear Markets but they are a natural part of the market cycle. As of September 15th, 2022, the NASDAQ is down 27.11% and the S&P 500 is down 18.15%. None of our portfolios are down this much.

Conclusion

Our income portfolios are built to withstand 5 to 6 years of a Bear Market (which has never happened in history) assuming a maximum income withdrawal of 5% per year which is inline with standard recommendations for income withdrawals. These include Ultra Conservative, Conservative, and Moderate portfolios as withdrawals are taken from cash and fixed income holdings first. Including the Great Depression, the longest Bear Market in history (the Dot Com Bubble) lasted 2.5 years1.

We have bought back into some equities while many have been “on sale” but you will not see the benefits of these adjustments until perhaps the middle of next year or when we return to a Bull Market. This strategy is intended to enhance overall long-term returns but NOT in the short-term. Patience is key. Over the past 73 years, the shortest bear market was three (3) months and the longest was 25 months2. The wise thing is to not panic and stay disciplined during times like this.

If you would like more information, please read our Bear Market Newsletter articles by clicking the following link. https://testing.christianfinancialadvisors.com/tag/2022-may/

As always, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss any of the above, please feel free to respond by emailing us or text/call us at 830-609-6986.

Bob Barber

CEO, Christian Financial Advisors®

Shawn Peters

CCO, Christian Financial Advisors®

1 https://www.nytimes.com/2022/06/13/business/bear-market-timeline-stocks.html

2 https://christianfa-website.storage.googleapis.com/wp-content/uploads/20260203144651/staying-invested-during-down-markets.pdf[/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

Mid-April 2022 Market Commentary

First Things First

In the last few weeks, we’ve seen a large influx of prospective clients the likes of which we haven’t seen in a long time. In my many years of experience, this is a good and bad thing because this happens every time I have seen a prolonged bear/down market as people start hunting for greener pastures. Contrary to popular opinion the grass is not greener on the other side. We have not lost a single client this year so far but are gaining so many new clients it concerns me. I have seen this happen over and over as people move from Advisor A in a down market to Advisor B and clients from Advisor B move to Advisor A. During times like this be very, very careful of chasing returns. No advisor controls the stock or bond markets.

What a difference one month makes!

The Positives

The Ukrainian/Russian war continues but is no longer front-page news, gasoline prices are way off their highs and stabilizing, Unemployment is at lows not seen in years as people get back to work post-COVID, leisure travel is returning swiftly, airlines are full and all the cruise lines are at record bookings, and the list goes on.

The Negatives

Inflation! Need I say more? If yes, “too many dollars chasing too few goods”.

The stock market year to date

While the overall stock and bond markets are still down year-to-date, 80-85% of the decline occurred in January. When you look at this on a graph it looks like a 45-degree downward line in January and a 2-3 degree downward line since January.

As I said in last month’s commentary, six months ago, way before the large drop in the markets in January, we thankfully sold off many of our equity/stock positions in our portfolios and held the proceeds in cash and short-term bond positions waiting for a buying opportunity at much lower prices. In February we bought back some of those equities/stock positions at much lower prices than we sold them for just 4-6 months earlier. We still have much more to go to get back to our normal allocation in equities/stock positions in our portfolios but are waiting patiently for a few more buying opportunities. In the long-term, this has the potential to greatly enhance our overall returns but NOT in the short-term until the markets get back to normal. Patience is key in times like this while waiting for the markets to return to normal. Over the past 73 years, the shortest recovery time was three (3) months, and the longest was 25 months. The wise thing is to not panic and stay disciplined.

The keys to investing right now, and as always, are as follows:

- A sound mind

- Wisdom

- Patience

- Time

Emotions should have no part in well thought out, long-term investment decisions.

2 Timothy 1:7

For God has not given us a spirit of fear, but of power and of love and of a sound mind.

Proverbs 9:12

If you are wise, your wisdom will reward you; if you are a mocker, you alone will suffer.

Galatians 5:22-23

But the fruit of the Spirit is love, joy, peace, patience, kindness, goodness, faithfulness, gentleness, self-control; against such things there is no law.

Ecclesiastes 3:1-3

There is a time for everything, and a season for every activity under the heavens: a time to be born and a time to die, a time to plant and a time to uproot, a time to kill and a time to heal, a time to tear down and a time to build,

To reiterate what I said in my last commentary, in the next 6-18 months we could see:

- Lower inflation as the Covid stimulus of over 9 trillion dollars from the government and the federal reserve subsides.

- Real Estate at more affordable prices as artificially low-interest rates start returning back to normal with the Federal Reserve raising rates along with stopping their program of buying over a hundred billion dollars a month in mortgage-backed bonds that further created a massive real estate bubble with high liquidity. We are already starting to see this in different parts of the country as long-term 30-year mortgage rates have gone from the low 3% range to the low 5% range. Whatever you do right now, do not buy real estate! In my opinion, we have a bubble bigger than 2008, and I have been a major real estate investor for 37 years with a lot of success. It is a time to be patient and wait for prices to adjust over the next 12-24 months to higher interest rates and a tighter mortgage market. It’s just math.

- Manufacturing in the United States is starting to return back to post-COVID levels.

- The chip shortage that has caused major disruptions in automobile manufacturing along with other businesses should be subsiding in the next 6-18 months.

- The jammed-up supply chain is opening back up and hopefully will return back to normal soon.

- COVID is moving to an endemic status.

- Oil prices are already easing as more supply comes online from the motivation to drill at today’s high prices.

- Markets should return to normal growth rates possibly by the end of this year, or before, but not the kind of growth rates we saw in the last few years from the massive 9+ trillion dollars of artificial stimulus the government and federal reserve provided.

- Hopefully, an end will come soon to the Ukrainian/Russian War. The stock markets do not really care which side wins, it just doesn’t like the uncertainty. However, as Christians, we do care and should pray earnestly for the Ukrainians and provide support in any way we can to fight tyranny.

During times like these, it is important to consider the seven questions from our article “Questions to ask when the markets are down” (click here to read it).

To see two very good charts on staying invested during down markets CLICK HERE.

In closing, if you have still not seen the webinar Shawn and I did online in February I would encourage you to do so by CLICKING HERE.

As always, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss any of the above, please feel free to respond by emailing us or text/call us at 830-609-6986.

Bob Barber

CEO, Christian Financial Advisors®

Shawn Peters

CCO, Christian Financial Advisors® [/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

Mid-March 2022 Market Commentary

The Ukrainian/Russian war, Iran’s missile launch a few days ago, high gasoline prices not seen in 8 years, rampant inflation from over 9 trillion dollars in stimulus packages the last few years, political instability, and extreme volatility in the stock and bond markets. If it all sounds quite concerning, it is and it can be very emotional. However, as Christians, we should never put our faith in man or emotions, but instead in God and his Word. Here is one of my favorite scriptures and I believe it is very applicable for times like this.

Ecclesiastes 3:1-8 There is an appointed time for everything. And there is a time for every matter under heaven—A time to give birth and a time to die; A time to plant and a time to uproot what is planted. A time to kill and a time to heal; A time to tear down and a time to build up. A time to weep and a time to laugh; A time to mourn and a time to dance. A time to throw stones and a time to gather stones. A time to embrace and a time to shun embracing. A time to search and a time to give up as lost; A time to keep and a time to throw away. A time to tear apart and a time to sew together; A time to be silent and a time to speak. A time to love and a time to hate; A time for war and a time for peace.

This scripture reminds us that nothing stands still, life is always in motion and we should not be surprised by wars and bad times as well as times of peace and prosperity.

Oil and Gasoline prices

Over the last week, oil and gas prices have fluctuated by as much as 20-30% from day-to-day putting gasoline prices back to what we were paying at the pump between 2008-2014 before record amounts of oil were discovered through fracking. Now with oil prices once again over $100 a barrel, companies are very motivated to bring more oil online which historically increases supply and drive prices back down. To see a chart of historic oil prices, CLICK HERE. To see a chart of historic gas prices CLICK HERE. Both of these historic charts may surprise you what we were paying for oil and gas just 8-12 years ago, but we forget.

The stock market year to date

With all this news, many well-known companies’ stocks are down 30-50% year to date.

Thankfully six months ago, way before the large drop in the markets, we sold off many of our equity/stock positions in our portfolios and held the proceeds in cash and short-term bond positions waiting for a buying opportunity like now at much lower prices. Recently we bought back many of the equities/stock positions at much lower prices than we sold them for just 4-6 months ago. We still have more than our normal allocation in cash and short-term bonds to buy more before returning to our normal allocation in equities/stock positions in our portfolios. In the long-term, this should greatly enhance our overall returns but NOT in the short-term until the markets get back to normal. Patience is the key in times like this while waiting for the markets to return to normal, which sometimes can be a short period of time, other times possibly as long as 1-3 years. The wise thing is not to panic when markets are resetting which is normal every few years.

What’s possible in the next 6-18 months?

- Lower inflation as the Covid stimulus of over 9 trillion dollars from the government and the federal reserve subsides.

- Real Estate at more affordable prices as artificially low-interest rates start returning back to normal with the Federal Reserve raising rates along with stopping their program of buying over a hundred billion dollars a month in mortgage-backed bonds that further created a massive real estate bubble with so much liquidity. Whatever you do right now, do not buy real estate! In my opinion, we have a bubble bigger than 2008, and I have been a major real estate investor for 37 years with a lot of success. It is a time to be patient and wait it out for prices to adjust over the next 12-24 months to higher interest rates and a tighter mortgage market. It’s just math.

- Manufacturing in the United States should return back to normal as covid subsides along with covid unemployment benefits ending.

- The chip shortage that has caused major disruptions in automobile manufacturing along with other businesses should be subsiding in the next 6-18 months.

- The jammed-up supply chain is opening back up and hopefully will return back to normal soon.

- COVID is moving to an endemic status.

- Oil prices should ease as more supply comes online from the motivation to drill at today’s high prices.

- Markets should return to normal growth rates but not the kind of growth rates we saw in the last few years from the massive 9 plus trillion dollars of artificial stimulus the government and federal reserve provided.

- Hopefully, an end will come soon to the Ukrainian/Russian War. The stock markets do not really care which side wins, it just doesn’t like the uncertainty. However, as Christians, we do care and should pray earnestly for the Ukrainians and provide support in any way we can to fight tyranny.

During times like this, it is important to think of the following questions.

- Will I need absolutely everything in my diversified investment portfolio in the next 1 to 3 years to live on? If not, you’re good.

- Do I have enough funds that are NOT in stocks and equities to last me for the next 3 to 5 years to live on while waiting for the stock portion of my portfolio to recover? Note: Our moderate portfolio has as much as 40 to 60% in fixed income, which allows the stock market portion of the portfolio to recover over time.

- Am I smart enough to perfectly time the market by getting out at the perfect time and getting back in at the perfect time? Note: just missing 3-5 days of positive market returns in a month can affect overall performance dramatically.

- Do I believe my well-diversified portfolio in things people use daily like technology, healthcare, medicine, utilities, gas, transportation, food, shelter, clothing, etc. will no longer be needed in the short term?

- Will I allow “short-term thinking” to get in the way of long-term success?

- Should I look at the markets when they are down as a possible buying opportunity instead of a selling one?

- Do great investors like Warren Buffet go with the crowd and run away from the markets when they are correcting or buy more at lower prices?

To see two very good charts on staying invested during down markets CLICK HERE.

In closing, if you have still not seen the webinar Shawn and I did online a few weeks ago I would encourage you to do so by CLICKING HERE.

As always, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss any of the above, please feel free to respond to this email or text/call us at 830-609-6986.

Bob Barber

CEO, Christian Financial Advisors®

Shawn Peters

CCO, Christian Financial Advisors® [/vc_column_text][vc_empty_space][vc_column_text][/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

February 25th, 2022 Market Commentary

As promised in the text we sent out this morning, with the world events that are unfolding at this time due to the Russia/Ukraine conflict and how this may affect the markets, here is the Market Commentary. We have also scheduled a webinar for Saturday, February 26th at 11am Central Standard time to allow us to go into more detail. Click here to reserve your spot.

The markets did not react nearly as negatively as many expected today from the Russian invasion of Ukraine. This could be partially due to the markets waking up to the fact that Ukraine’s GDP is ONLY approximately $155 billion annually and Russia’s is ONLY $1.5 trillion annually. The annual GPD for Texas alone is $1.75 trillion or, on the world stage, the U.S is $21 trillion, Japan $5 trillion, and Germany $3.7 trillion of GPD annually. In other words, Russia’s and Ukraine’s GDP combined is just not enough mathematically to make much of a difference at all. But, if Russia keeps going into neighboring countries and this turns into a world war it would be a different story. I do not believe this will happen because then Russia is against the world including superpowers that can defend themselves, unlike Ukraine.

There are many other underlying issues that have put the markets where they are today which I will provide in the webinar Saturday. Again, click here to reserve your spot.

With all this in mind, we are now in a great position to start taking advantage of buying opportunities which we have been waiting for since September of last year when we peeled off some of our equity positions when the markets were at all-time highs. We cannot let you know exactly when we will be adding to equity positions at much lower prices than when we sold but you will get a notice when we have made the moves.

In the meantime do not let short-term negative returns and panic get in the way of a long-term strategy.

Our Biblically Responsible Portfolio Positions at this time

- Aggressive Portfolios: typically 98% to 99% equity/stock positions are presently at 82.5% equity/stock positions with the remainder in cash.

This portfolio’s Risk Number2 is 75, which means the Acceptable Six-Month Risk is -16.63%. - Growth Portfolios: typically 80% equity/stock positions are presently at 66% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number2 is 67, which means the Acceptable Six-Month Risk is -14.18%. - Moderate Portfolios: typically 50% to 60% equity/stock positions are presently ONLY at 36% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number2 is 52, which means the Acceptable Six-Month Risk is -10.23%. - Conservative Portfolios: typically 20% to 25% equity/stock positions are presently ONLY at 20% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number2 is 45, which means the Acceptable Six-Month Risk is -8.14%. - Ultra Conservative Portfolios: never have equity/stock positions but are always in cash and fixed income.

This portfolio’s Risk Number2 is 37, which means the Acceptable Six-Month Risk is -6.11%.

In closing, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

Click here to see Our Seven Investment Management Principles.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss this, please email us or text/call us at 830-609-6986.

Bob Barber

CEO, Christian Financial Advisors®

Shawn Peters

Wealth Advisor, Christian Financial Advisors®[/vc_column_text][vc_empty_space][vc_column_text]1 GDP values obtained from both https://tradingeconomics.com/ukraine/gdp and https://worldpopulationreview.com/state-rankings/gdp-by-state.

2 All Risk Number volatility percentages are based on 95% Historical Probability for six months and are used by our firm to remain as objective as possible in our professional investment management decisions. These numbers are from Riskalyze, a professional, paid advisor tool we use as a firm.[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

February 1st, 2022 Market Commentary

January was a very emotional and speculative month for the markets as day traders reacted aggressively to the Federal Reserve and what it MAY do with interest rates between now and the end of the year and how they could affect the profitability of companies.

The Invesco QQQ Trust (QQQ), which represents NASDAQ stocks, was down over 8.5% in January, with actual stocks like Amazon, Home Depot, TESLA, and NetFlix all down 10% or more. Even the Vanguard Total Bond Market ETF (BND) and iShares Core US Aggregate Bond ETF (AGG), which represent the overall Bond markets, were down approximately 2%.

The following benchmarks, comparable to an equally-weighted moderate portfolio, would have been down approximately 5-6% year-to-date: iShares Core Moderate Allocation ETF (AOM), Vanguard LifeStrategy Moderate Gr Inv, Fidelity® Balanced (FBALX), and the T. Rowe Price Spectrum Moderate Allc (TRPBX). Our Biblically Responsible Moderate Portfolios, net of fees, were on par with these comparable benchmarks for January1. All Moderate client portfolios have earned an average of 9% per year over the last three calendar years, net of advisory fees1.

It is essential to reiterate the article “Questions to ask when the markets are down” during times like this. Please see those questions below:

- Will I need everything in my diversified investment portfolio for living expenses in the next 1 to 3 years?

- Do I have enough funds that are NOT in stocks and equities to last me for the next 3 to 5 years to live on while waiting for the stock portion of my portfolio to recover?

Note: A moderate portfolio has as much as 40% to 60% in fixed income, allowing the portfolio’s stock market portion to recover over time. - Am I smart enough to perfectly time the market by getting out at the perfect time and getting back in at the perfect time? Note: just missing 3-5 days of positive market returns in a month can affect overall performance dramatically.

- Do I believe in the short term that people will no longer need technology, healthcare, medicine, utilities, gas, transportation, food, shelter, clothing, and more?

Note: Our well-diversified portfolios consist of these types of companies. - Will I allow “short-term thinking” to get in the way of long-term success?

- Should I look at it as a buying opportunity instead of a selling one when the markets are down?

- Do great investors like Warren Buffet go with the crowd and run away from the markets when they are correcting, or do they buy these lower-priced stocks?

We have been underweighted in equities/stocks in all our portfolios and overweight in fixed income and cash way before the January downturn. This will allow for great buying opportunities when the time is right. Our current goal is to protect our portfolios as much as possible while staying mostly invested (see below present allocations). Trying to completely time the markets very seldom works.

We are starting to see some good buying opportunities in a few of our funds that are notoriously known for quickly recovering losses when they have been stretched this far from their highs. We will start moving back into our standard equity/stock allocations when we see one, or both, of the following occur:

- the sideways to downward trend begins to turn

- it makes financial sense to buy at much lower values for the long run.

Do not let short-term negative returns and panicking get in the way of a long-term strategy.

Our Biblically Responsible Portfolio Positions at this time

- Aggressive Portfolios: typically 98% to 99% equity/stock positions are presently at 82.5% equity/stock positions with the remainder in cash.

This portfolio’s Risk Number2 is 75, which means the Acceptable Six-Month Risk is -16.74%. - Growth Portfolios: typically 80% equity/stock positions are presently at 66% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number2 is 67, which means the Acceptable Six-Month Risk is -14.28%. - Moderate Portfolios: typically 50% to 60% equity/stock positions are presently ONLY at 36% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number2 is 53, which means the Acceptable Six-Month Risk is -10.28%. - Conservative Portfolios: typically 20% to 25% equity/stock positions are presently ONLY at 20% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number2 is 45, which means the Acceptable Six-Month Risk is -8.17%. - Ultra Conservative Portfolios: never have equity/stock positions but are always in cash and fixed income.

This portfolio’s Risk Number2 is 37, which means the Acceptable Six-Month Risk is -6.12%.

In closing, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

Click here to see Our Seven Investment Management Principles.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss this, please email us or text/call us at 830-609-6986.

Bob Barber

CEO, Christian Financial Advisors®[/vc_column_text][vc_empty_space][vc_column_text]1 Returns for portfolios generated using Panoramix Reporting software. Moderate portfolios for 2019, 2020, and 2021 resulted in 10.41%, 8.06%, and 5.53%, respectively, and YTD returns were -5.11% as of 01/31/2022.

2 All Risk Number volatility percentages are based on 95% Historical Probability for six months and are used by our firm to remain as objective as possible in our professional investment management decisions. These numbers are from Riskalyze, a professional, paid advisor tool we use as a firm.[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

January 2022 Market Commentary Update

When Covid-19 hit, the Federal Reserve and the government put over 8 trillion dollars into the economy to stimulate it. This influx created massive inflation, especially in real estate and a significant stock market rally. Now, the federal reserve is saying no more “Free Candy” as they pull back stimulus by way of:

- Higher interest rates over the next 18 months

- Tampering bond-buying by the billions in mortgage-backed securities over the next few months

- Reducing their balance sheet

With the reality of these actions sinking in, the stock markets are now reacting negatively.

The S&P 500 has been flat since September 2, 2021, The Dow since August 12, 2021, and the Nasdaq since July 8, 2021. All gains made between these dates for all three indexes have disappeared, and all three indexes are down year to date.

Our portfolios have been underweighted in equities/stocks and overweighted in fixed income and cash for some time now. Our current goal is to protect our portfolios as much as possible while staying mostly invested. See present allocations below. Trying to time the markets perfectly very seldom works.

We are starting to see some good buying opportunities in a few of our funds that are notoriously known for quickly recovering losses when they have been stretched this far from their highs. We will start moving back into our standard equity/stock allocations when we see one, or both, of the following occur:

- the sideways to downward trend begins to turn

- it makes financial sense to buy at much lower values for the long run.

Do not let short-term negative returns and panicking get in the way of a long-term strategy.

Our Biblically Responsible Portfolio Positions at this time

- Aggressive Portfolios: typically 98% to 99% equity/stock positions are presently at 82.5% equity/stock positions with the remainder in cash.

This portfolio’s Risk Number is 74*, which means the Acceptable Six-Month Risk is -16.41%. - Growth Portfolios: typically 80% equity/stock positions are presently at 66% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 66*, which means the Acceptable Six-Month Risk is -13.99%. - Moderate Portfolios: typically 50% to 60% equity/stock positions are presently ONLY at 36% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 52*, which means the Acceptable Six-Month Risk is -10.10%. - Conservative Portfolios: typically 20% to 25% equity/stock positions are presently ONLY at 20% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 44*, which means the Acceptable Six-Month Risk is -8.08%. - Ultra Conservative Portfolios: never have equity/stock positions but are always in cash and fixed income.

This portfolio’s Risk Number is 37*, which means the Acceptable Six-Month Risk is -6.07%.

*All Risk Number volatility percentages are based on 95% Historical Probability for six months and are used by our firm to remain as objective as possible in our professional investment management decisions. These numbers are from Riskalyze, a professional, paid advisor tool we use as a firm.

In closing, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

Click here to see Our Seven Investment Management Principles.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss, please email us or text/call us at 830-609-6986.

Bob Barber

CEO, Christian Financial Advisors®[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_row_inner][vc_column_inner][vc_column_text]

December 20, 2021 Market Commentary

Omicron Fears and the Federal Reserve. Possibly no “Santa Claus” rally!

The stock markets are presently reacting negatively to three realities it now faces:

- Last week, the Federal Reserve indicated it will begin tapering its bond-buying program in 2022. This tapering has given the markets and the economy artificial stimulation over the previous 18 months.

- The Federal Reserve also expects to raise interest rates three times in 2022 to attempt to curb inflation.

- It is currently unknown how bad the Omicron Covid variant may affect the economy in the short term.

Trailing returns from September 2, 2021 to mid-day on December 20, 2021, are now flat for most well-known stock indexes like the S&P 500, Dow, and Nasdaq. This means they have given up all the gains made from October to the middle of December.

We have been underweighted in equities/stocks in all our portfolios and overweight in both cash and fixed income for some time now. Our current goal is to protect our significant gains as much as possible from the last 18-24 months. We will start moving back into our standard equity/stock allocations when we see one, or both, of the following occur 1) the sideways to downward trend begins turning OR 2) it makes financial sense to buy at lower values for the long run.

Our Biblically Responsible Portfolio Positions at this time

- Aggressive Portfolios: typically 98% to 99% equity/stock positions are presently at 86% equity/stock positions with the remainder in cash.

This portfolio’s Risk Number is 74*, which means the Acceptable Six-Month Risk is -16.32%. - Growth Portfolios: typically 80% equity/stock positions are presently at 68% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 66*, which means the Acceptable Six-Month Risk is -13.93%. - Moderate Portfolios: typically 50% to 60% equity/stock positions are presently at 37% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 52*, which means the Acceptable Six-Month Risk is -10.06%. - Conservative Portfolios: typically 20% to 25% equity/stock positions are presently at 19% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 44*, which means the Acceptable Six-Month Risk is -8.07%. - Ultra Conservative Portfolios: never have equity/stock positions but are always in cash and fixed income.

This portfolio’s Risk Number is 37*, which means the Acceptable Six-Month Risk is -6.08%.

*All Risk Number volatility percentages are based on 95% Historical Probability for six months and are used by our firm to remain as objective as possible in our professional investment management decisions. These numbers are from Riskalyze, a professional, paid advisor tool we use as a firm.

In closing, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

Click here to see Our Seven Investment Management Principles.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss, please reply to this commentary by email or text/call us at 830-609-6986.

Have a Merry Christmas,

Bob Barber

CEO, Christian Financial Advisors®

P.S.

Special Hours of Operation

Our physical office will be closed from noon on Tuesday, December 21st until after Christmas; however, we will be working remotely and accepting phone calls, text messages, and emails for service requests until December 24th at noon.

After Christmas, our physical office will be closed starting Wednesday, December 29th until after New Year’s Day; however, we will be working remotely and accepting phone calls, text messages, and emails for service requests until December 31st at noon.

Regular hours resume on Monday, January 3rd, 2022 for both in-office and remote service requests.[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]

[vc_row top=”20px” bottom=”20px”][vc_column][vc_single_image image=”12107″ img_size=”Full” alignment=”center”][vc_row_inner][vc_column_inner][vc_column_text]

December 7, 2021 Market Commentary

As of last week, three-month trailing returns for most of the well-known stock indexes like the S&P 500, Dow, and Nasdaq were all basically flat, giving up all gains made in October and November. See more details below on our portfolios’ present positions.

Our Biblically Responsible Portfolio Positions at this time

- Aggressive Portfolios: typically 98% to 99% equity/stock positions are presently at 86% equity/stock positions with the remainder in cash.

This portfolio’s Risk Number is 72*, which means it could be down 15.76% or up 25.33%. - Growth Portfolios: typically 80% equity/stock positions are presently at 68% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 62*, which means it could be down 12.90% or up 20.93%. - Moderate Portfolios: typically 50% to 60% equity/stock positions are presently at 37% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 44*, which means it could be down 8.05% or up 14.02%. - Conservative Portfolios: typically 20% to 25% equity/stock positions are presently at 19% equity/stock positions with the remainder in cash and fixed income.

This portfolio’s Risk Number is 37*, which means it could be down 6.03% or up 10.61%. - Ultra Conservative Portfolios: never have equity/stock positions but are always in cash and fixed income.

This portfolio’s Risk Number is 29*, which means it could be down 3.85% or up 7.38%.

*All Risk Number volatility percentages are based on 95% Historical Probability for six months and are used by our firm to remain as objective as possible in our professional investment management decisions. These numbers are from Riskalyze, a professional, paid advisor tool we use as a firm.

As you can tell from our above allocations, we are presently underweighted in equities/stocks, overweight cash/fixed income. Our goal at this time is to protect our clients’ large gains made over the last 18 months from all the trillion of dollars in artificial stimulus given to the economy by the government because of Covid-19. We will start moving back into our normal equity/stock allocations when we see the sideways trend turning, if it makes financial sense to buy at lower values for the long run or a combination of both.

We may see what is typically called a “Santa Claus rally” in December in the next three weeks, but this will probably be a complete head fake just like October and November were in the markets and could be given up in January. I’ve seen the markets do this many times in my experience.

Over the last 18 months, the Federal Reserve has put 120 billion dollars into the bond markets to stimulate the economy. Last week, Federal Reserve Chairman Jerome Powell indicated an acceleration of their timetable to reduce their ongoing bond market stimulation while also raising interest rates sooner than initially expected. The goal of the Fed is to have no new net purchases of bonds by mid-2022, but the path to this goal will depend on economic developments.

One outcome we may see when all the artificial stimulus of trillions of dollars diminishes and artificially low mortgage rates return to normal is a highly overinflated real estate market drop to more realistic levels. Real estate has seen 25-40% inflation in just the last year, and therefore many markets could dramatically drop to compensate. Real estate buyers need to consider if they would rather owe more by buying now at lower rates or owe less by buying later at higher rates if the mortgage payment could be the same. DISCLAIMER – In theory, lower interest rates normally equal higher prices, higher interest rates normally equal lower prices, but this is not always the case. Only history will tell if it’s different this time.

In closing, rest assured we are consistently monitoring events, the markets, and all our portfolios hourly, daily, and many times into the late evenings as well as very early in the mornings for your benefit as our clients.

Click here to see Our Seven Investment Management Principles.

As a Fiduciary-based firm, we act as your trusted financial advocate for you. We are here to serve you, not the other way around.

If you would like to discuss, please reply to this commentary by email or text/call us at 830-609-6986.

Here to serve,

Bob Barber

CEO of Christian Financial Advisors®

P.S. Let us not forget that it was 80 years ago today, December 7, 1941, that the Japanese surprisingly attacked the U.S. naval base at Pearl Harbor on Oahu Island, Hawaii, that precipitated the entry of the United States into World War II. The next day President Franklin D. Roosevelt said those famous words “…a date which will live in infamy in the United States of America…”[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row]